Rev’s Transcript Library

Explore our extensive collection of free transcripts from political figures and public events. Journalists, students, researchers, and the general public can explore transcripts of speeches, debates, congressional hearings, press conferences, interviews, podcasts, and more.

Trump and Macron speak at G7 Summit

Donald Trump meets with French President Emmanuel Macron during the G7 summit. Read the transcript here.

Gavin Newsom Statement on DOJ Investigation

California Governor Gavin Newsom responds to the DOJ's investigation of him and his wife. Read the transcript here.

Sports Broadcasting Act Hearing

OutKick Media President Clay Travis testifies before the House on the Sports Broadcasting Act. Read the transcript here.

Secure America Act

Donald Trump signs the $70 billion Secure America Act for immigration enforcement. Read the transcript here.

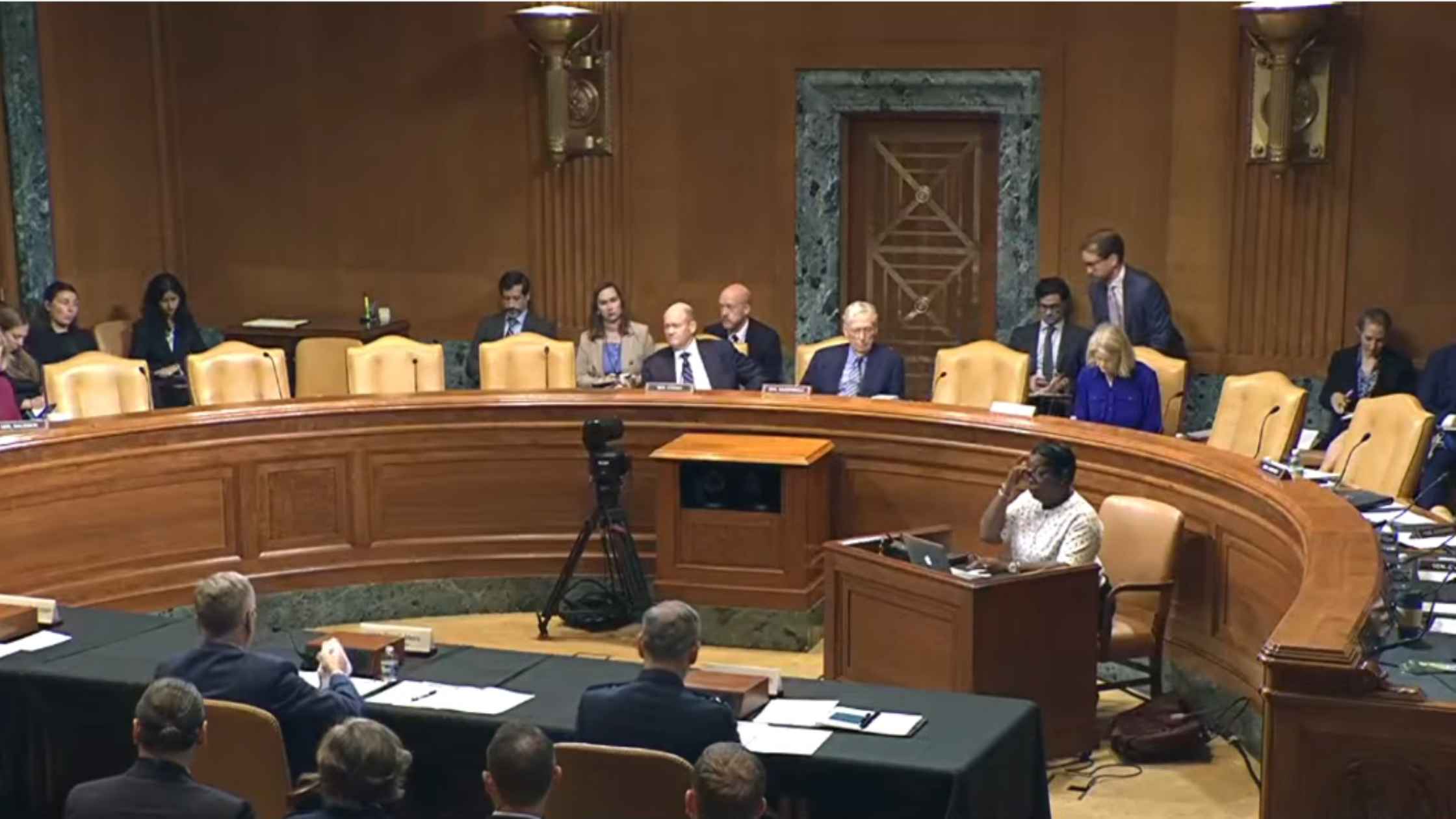

Air Force Senate Hearing

Air Force Secretary Troy Meink testifies before the Senate Appropriations Committee. Read the transcript here.

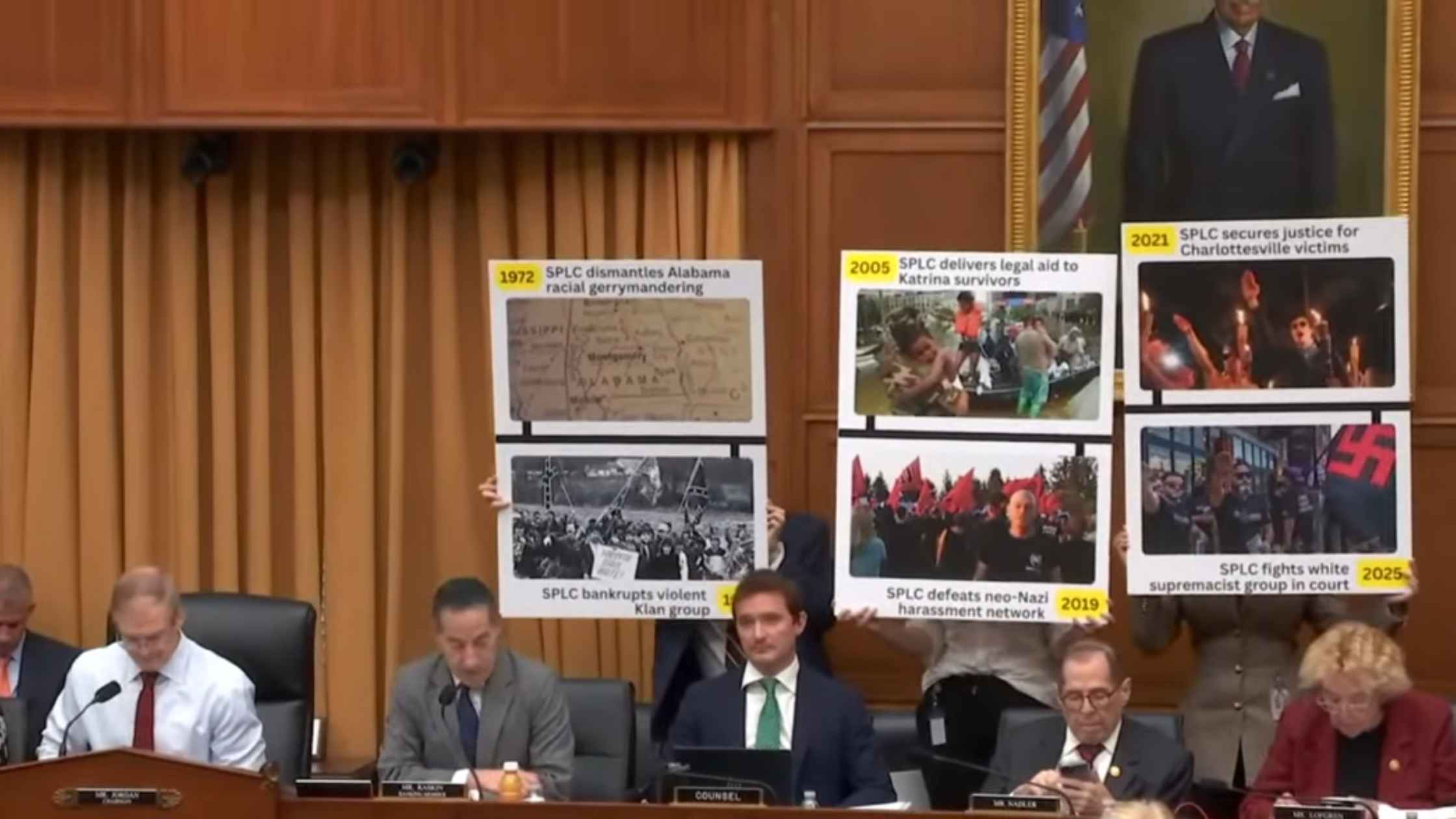

SPLC Hearing

Southern Poverty Law Center probed by the House Judiciary Committee. Read the transcript here.

ICE Funding Hearing

ICE funding bill is debated in the House Rules Committee. Read the transcript here.

Federal Reserve and FDIC Hearing

Federal Reserve and FDIC officials testify on financial regulation in a House hearing.

House Agriculture Hearing

Brooke Rollins testifies on USDA priorities in a House Agriculture hearing. Read the transcript here.

Coal Industry Announcement

Donald Trump makes an announcement about the coal industry in the Oval Office. Read the transcript here.

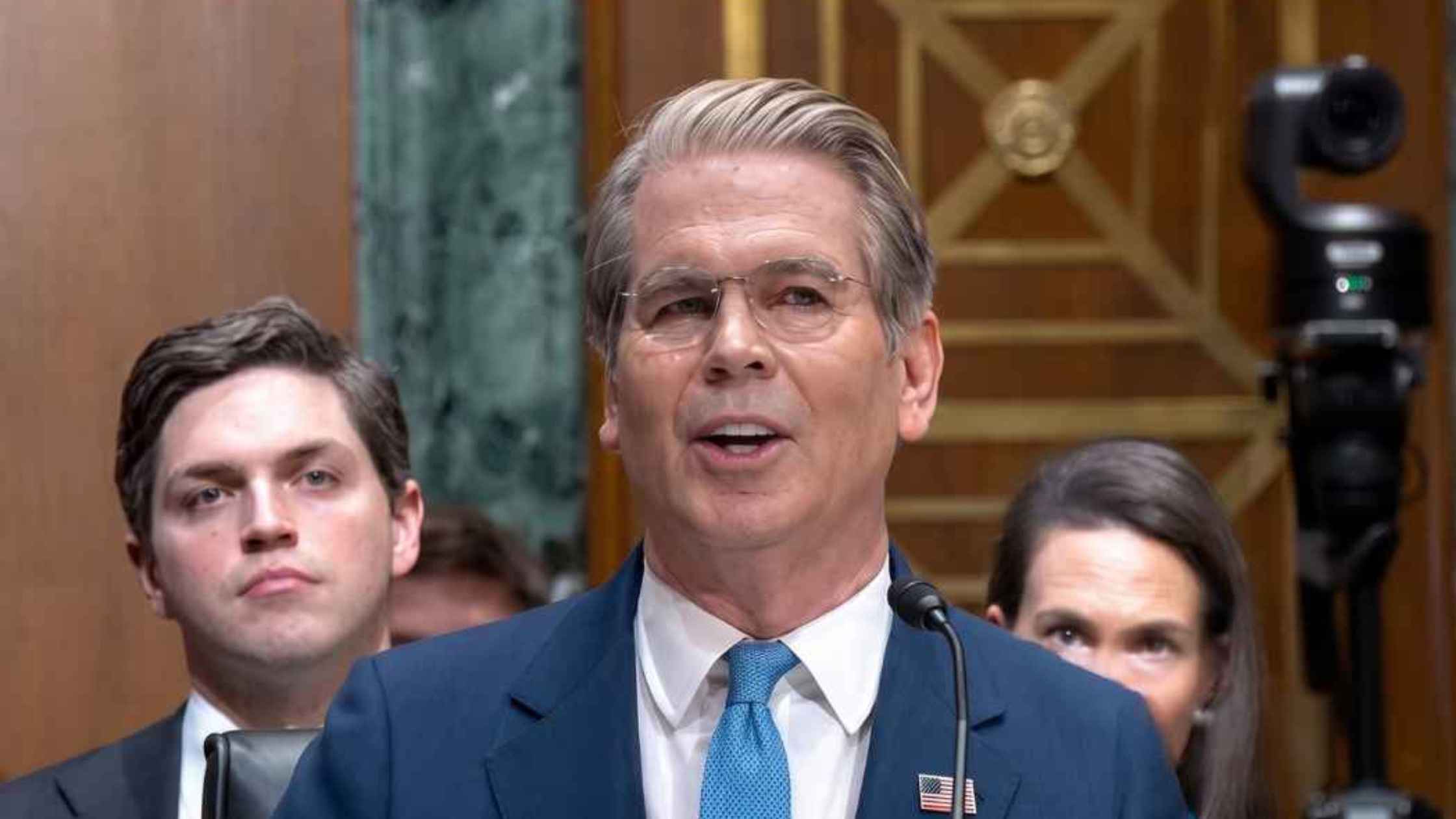

Senate Finance Committee Hearing

Treasury Secretary Scott Bessent testifies before the Senate Finance Committee. Read the transcript here.

Rubio Testifies Before Senate Foreign Relations Committee

Secretary of State Marco Rubio testifies before the House Foreign Affairs Committee on the State Department's 2027 budget request. Read the transcript here.

Subscribe to The Rev Blog

Sign up to get Rev content delivered straight to your inbox.