Business Content & Transcripts

How to Take Better Notes at Work

Business Content & Transcripts

Cybersecurity For Law Firms: How To Avoid A Breach

Learn how to improve your law firm’s cybersecurity with key threats, compliance rules, and 10 practical strategies to protect sensitive client data.

ADA Website Compliance: What Site Owners Need to Know

Learn about upcoming ADA website compliance deadlines for schools, public agencies, and site owners. Plus, download our checklist to ensure your site is accessible.

Insurance Transcription: 5 Services for Claims + Compliance

Take a look at the top insurance transcription services that understand insurance workflows and can handle even the most sensitive investigation recordings.

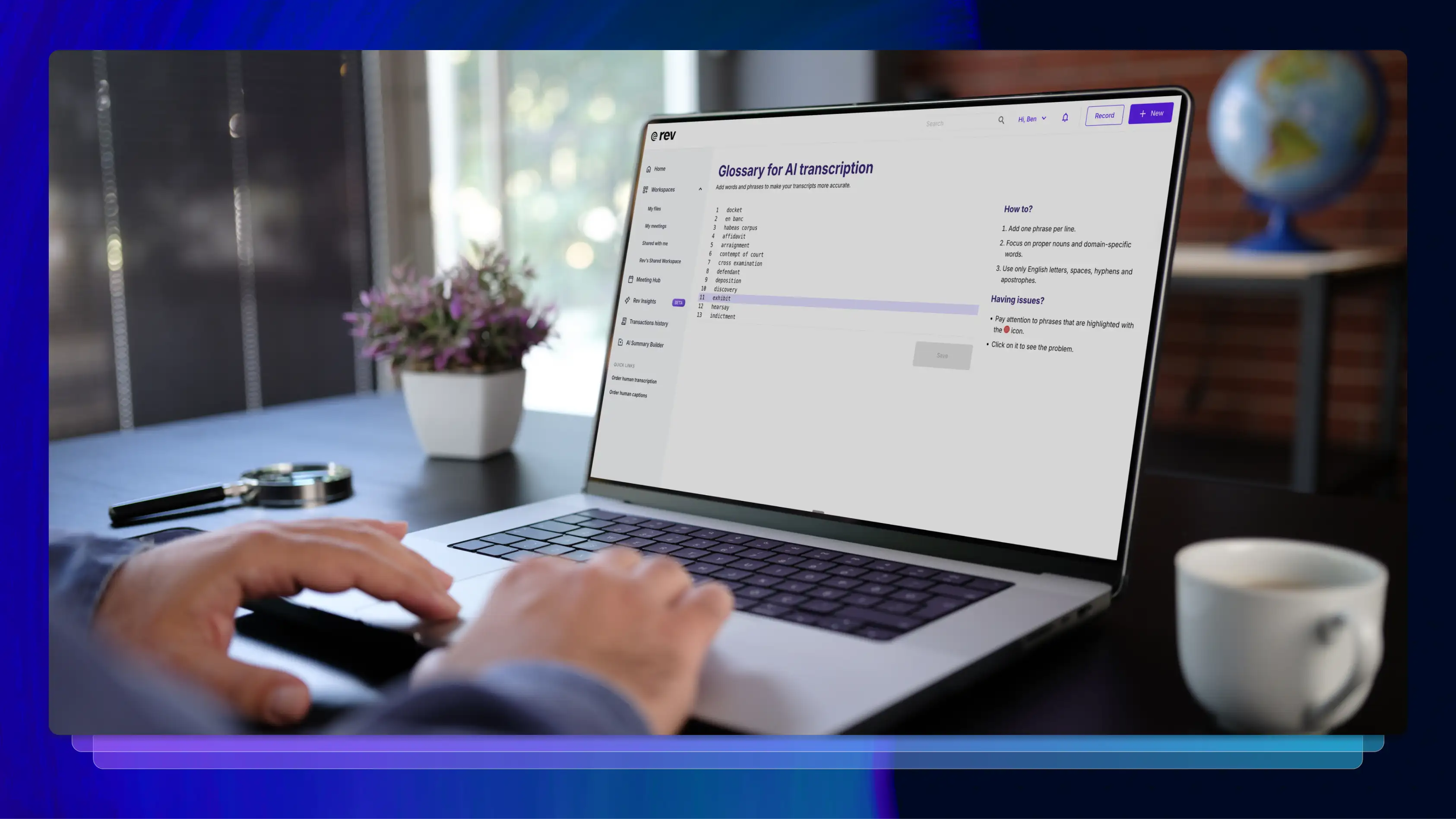

100+ Legal Terms + How A Transcript Glossary Improves Accuracy

Explore 100 essential legal terms and learn how Rev’s custom glossaries improve transcript accuracy, consistency, and efficiency for legal teams.

2026 New Year's Resolutions for Lawyers + Law Firms

Wanting to level up your practice in the new year? Here are some New Year’s resolutions for attorneys and law firms to help you boost productivity and win more cases.

85% Believe Prompting Will Be a Must-Have Job Skill in the AI Era

A new survey reveals Gen Z treats AI prompting as career prep, while employer training boosts efficiency 20%. See how generations approach this emerging job skill.

What Is Legal Operations? + Tips To Manage My Firm's Legal Ops

Legal operations is a critical component of a successful law practice. Learn how to implement the right legal ops solutions at your firm in this guide.

What Does a Paralegal Do?

Paralegals play a critical role in legal work, supporting attorneys in everyday tasks. Learn what a paralegal does, how to become one, and how tech can help.

Usability Testing Strategies + Process

Here’s Rev’s guide to everything you need to know about usability testing and UI testing, including UX testing strategies and potential test questions.

Transcription Outsourcing Benefits + Features To Look For

Save time and improve accuracy by outsourcing transcription. Learn how to choose reliable services and manage your workflow efficiently.

How to Transcribe Meeting Minutes for Better Note-Taking

A step-by-step guide detailing how to transcribe meeting minutes for better note-taking using transcribing software.

10 Best Note-Taking Apps For iPads

Turn your iPad into the ultimate notebook. Discover 10 top note-taking apps for iPad that offer handwriting, typing, and cloud sync to stay organized.

11 Better Fireflies.ai Alternatives

Looking for an alternative to Fireflies.ai notetaker? We’ve compiled 11 of the best AI-powered note-taking services that can help you uplevel your meetings and gather great insights.

How to Take Better Notes at Work

Note-taking skills are critical in the business world. Learn how to take faster and better notes — and the tools that can help you do it.

Cybersecurity Risk Assessment: What It Is and How To Get Started

Rev explains what cybersecurity risk assessment is and how to get started implementing it to ensure that your company and all its assets are covered.

Data Security Management 101

Data security management is now a top priority for most organizations. Here’s what you need to know to ensure you have the right data safeguards in place.

Why Is Time Management Important?

Why is time management so important? Effective time management allows for more productivity, better focus, and ultimately, better work. Rev tells you how!

How to Securely Send Important Documents via Email

Cybersecurity is becoming more and more prominent as technology continues to grow. Let’s take a look at how to send a secure email, how to password protect an email, and how to make sure your documents arrive safely to their digital destination.

.webp)

Managing Risk Mitigation (Strategies and Tools You Need Now)

Business risk management is all about being proactive. In this article we explore what risk mitigation is, common risk mitigation strategies companies may employ, and tools they can use to help do it.

8 Zoom Alternatives For Virtual Meetings in 2026

Zoom isn’t the only video meeting platform on the market. Here are eight competing apps to try for your online meetings and conference calls.

The Best AI Productivity Tools to Simplify Your Workday

Rev breaks down eight AI productivity tools that make your job easier, your team more productive, and every project better.

Digital Note-Taking 101: Take Notes With Ease

Switch to digital note-taking. Learn tools and techniques to organize and access your notes more efficiently across devices.

Video SEO: How to Increase Video Views and Rankings

Video SEO can greatly improve the rankings of your video content. Let’s look at what makes a good video and how to incorporate it into your SEO work.

11 Meeting AI Tools For Boosting Productivity

Discover 11 AI-powered meeting tools that transcribe discussions, summarize key points, and automate follow-ups to make meetings more productive.

Never Miss a Meeting: How Meeting Notetakers Boost Productivity in the Digital Age

Discover how meeting notetakers boost productivity. Learn key features, best practices, and how to leverage these tools for seamless collaboration.

Boosting Team Productivity with Meeting Notetakers

Boost team productivity with meeting notetakers. Learn how these tools enhance collaboration and knowledge sharing.

8 CoPilot Alternatives

Check out Rev’s breakdown of the best Microsoft Copilot alternatives designed to streamline your workflow and boost productivity, including our new platform.

40 Meeting Statistics That Showcase New Trends in Meetings

Let’s look at some must-know meeting statistics to learn more about the advantages of meetings and when they’re unnecessary.

12 Team Collaboration Tools to Boost Productivity and Innovation

Make teamwork easier with better software. Discover 12 top collaboration tools for project management, chat, and file sharing to boost team productivity.

Expert Insight to Boost Workplace Productivity

Boost your workplace productivity with these 7 proven tips. Improve focus, manage time better, and get more done every day.

9 Best Note-Taking Apps to Make Your Life Easier

Taking notes is an intensely specific and important process, and Rev is here to help you choose the best note-taking app to make life easier.

Rev vs. Otter: Which is Better for Your Productivity Needs?

Learn everything you need to know about Rev vs. Otter—including which service is right for you and your productivity needs.

AI Efficiency: Four Ways AI Helps Your Business Productivity

Learn how to work smarter with AI. See how artificial intelligence can automate routine tasks and analyze data, helping you accomplish more.

Workflow Automation: What It Is + 10 Automation Apps You Need

Workflow automation can revolutionize your day, whether you’re a company or a content creator. Here are 10 workflow automation apps you need.

How to Start a Podcast With No Audience: It Can Be Done!

If you’re wondering how to start a podcast audience with no audience, rest assured: It can be done! And Rev will tell you how in 12 steps.

Film & Television Set Security Best Practices

A film set can be a chaotic place. Learn film and television set security best practices to protect your people and their work.

Warner Bros Discovery Q1 2026 Earnings Conference Call

$WBD Warner Bros Discovery Q1 2026 earnings conference call. Read the transcript here.

Hegseth at Bath Iron Works

Defense Secretary Pete Hegseth speaks at Bath Iron Works. Read the transcript here.

Newsom at Davos

California Governor Gavin Newsom speaks at the World Economic Forum in Davos. Read the transcript here.

Merz at Davos

German Chancellor Friedrich Merz gives a special address at the World Economic Forum in Davos. Read the transcript here.

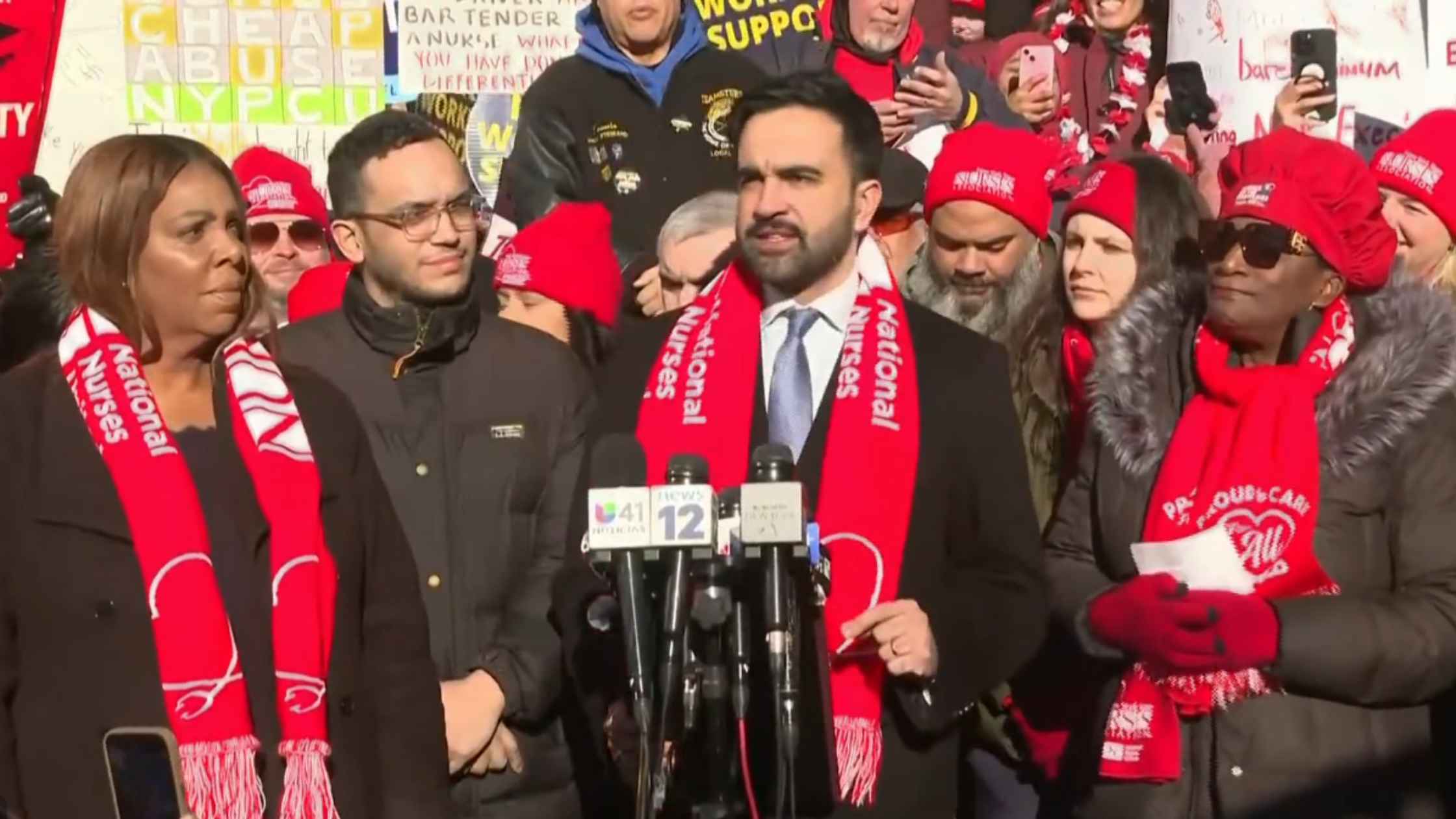

Nurse Strike Press Conference

A press conference was held as thousands of nurses at several major New York City hospitals went on strike. Read the transcript here.

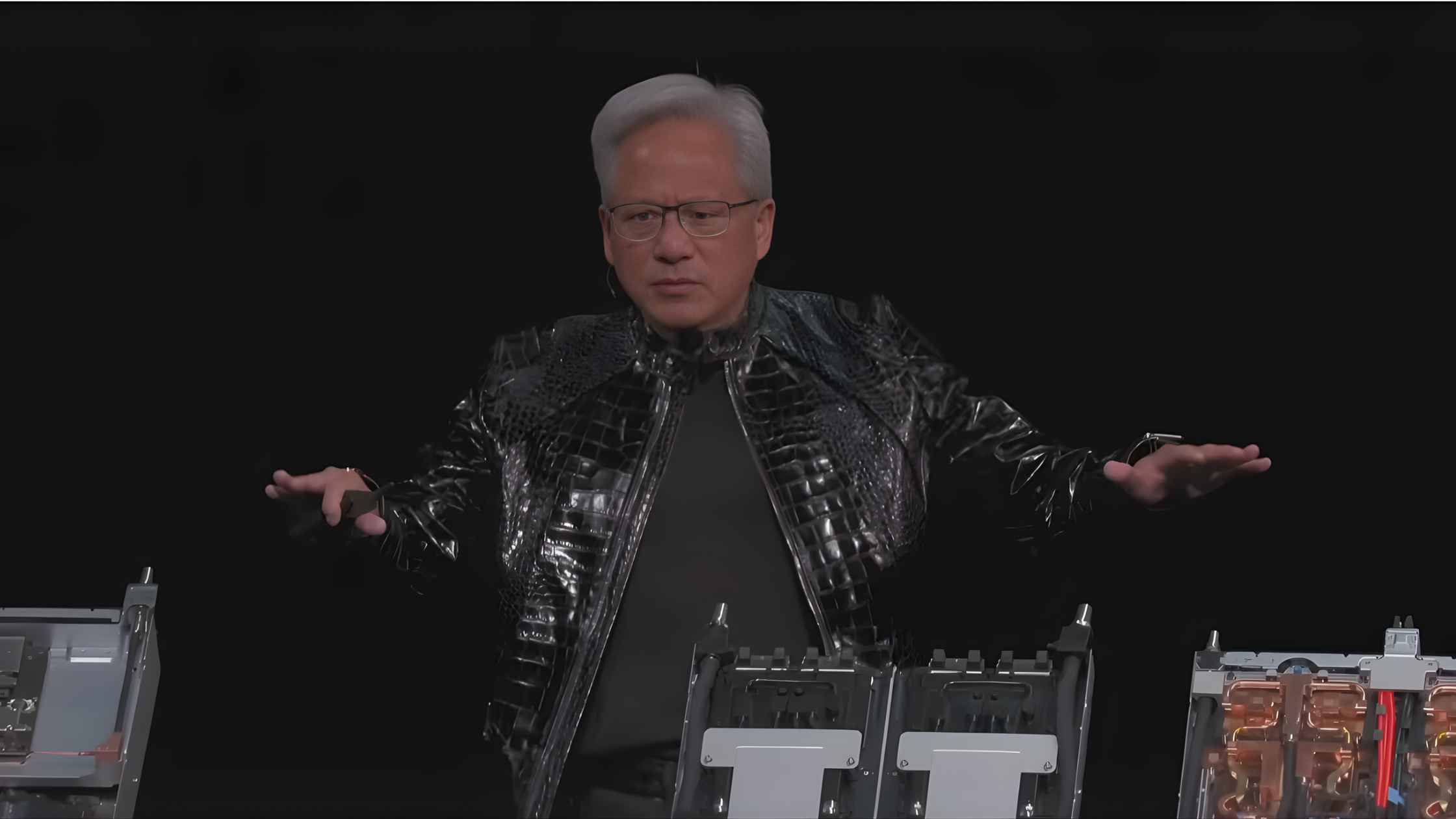

NVIDIA at CES 2026

NVIDIA founder and CEO Jensen Huang speaks at the Consumer Electronics Show in Las Vegas. Read the transcript here.

Federal Reserve Chair Jerome Powell Speaks After Rate Cut

Jerome Powell holds a briefing after the Federal Reserve cut interest rates in another divided vote. Read the transcript here.

Nvidia CEO Fireside Chat

NVIDIA founder and CEO Jensen Huang participates in a fireside chat on securing U.S. leadership in Artificial Intelligence. Read the transcript here.

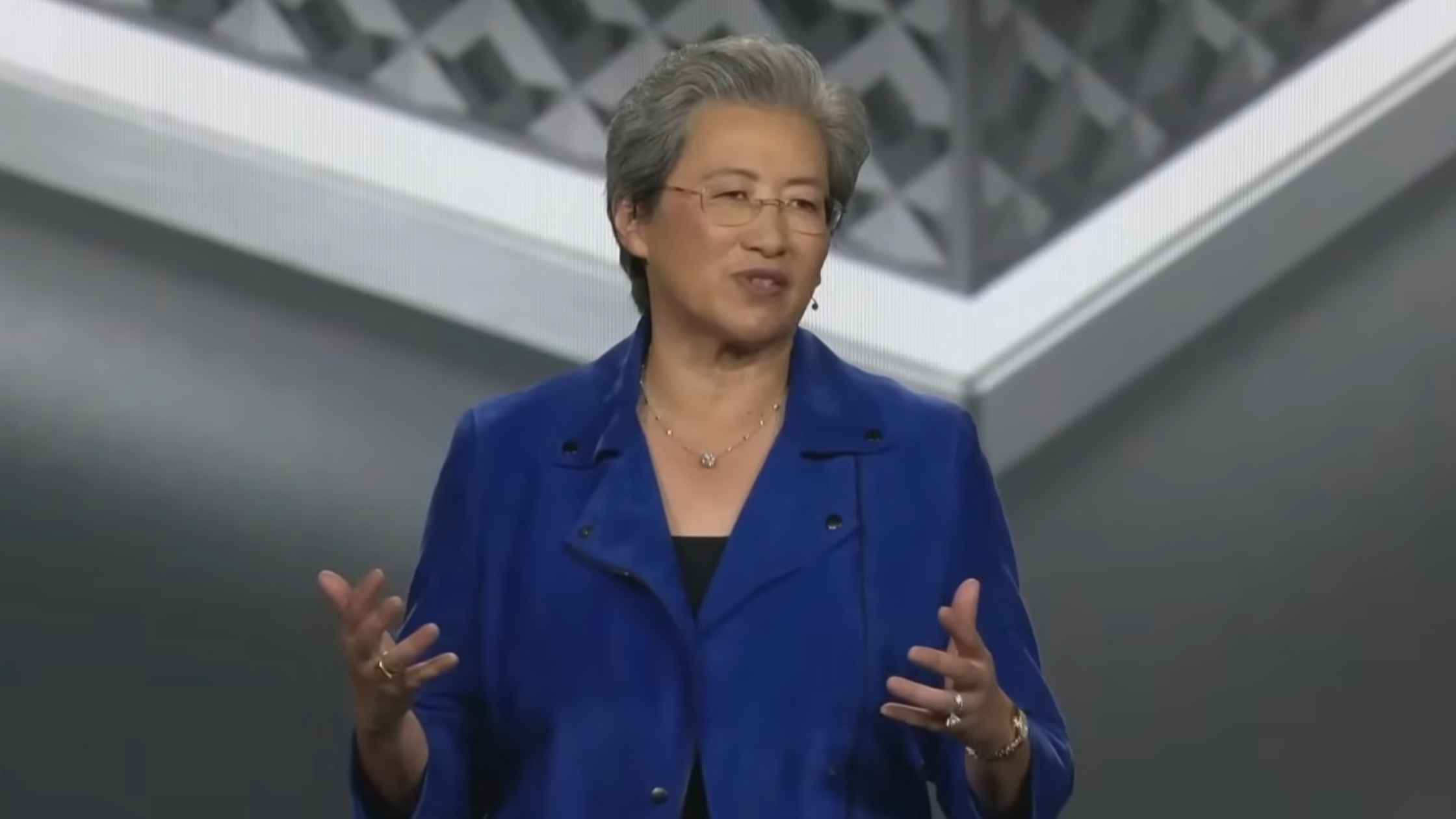

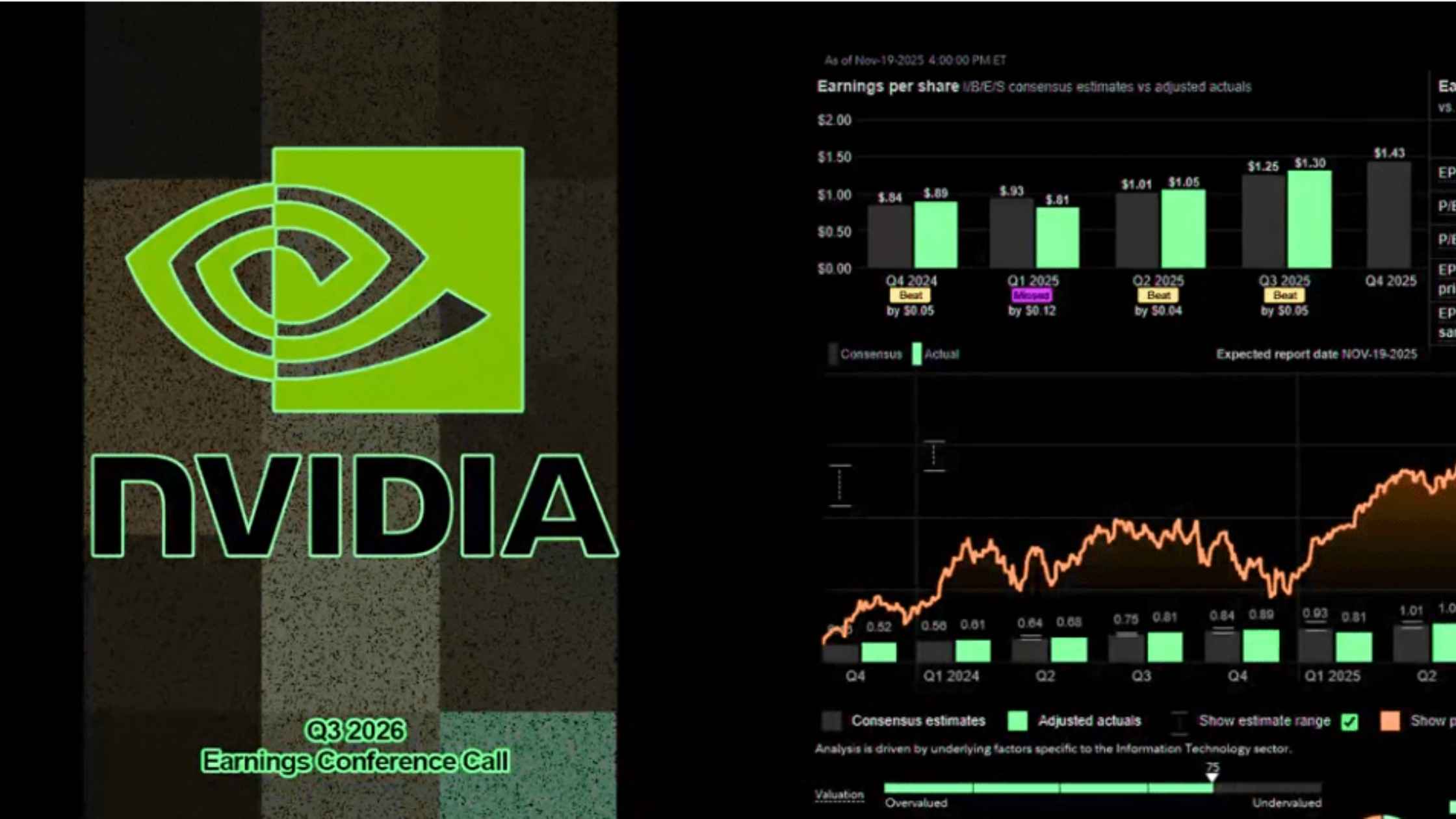

NVIDIA Q3 2026 Earnings Conference Call

$NVDA NVIDIA Q3 2026 Earnings Conference Call. Read the transcript here.

Fed Chair Lowers Interest Rates

Jerome Powell delivers remarks after the Federal Reserve cuts interest rates. Read the transcript here.

Mark Cuban Testifies on Healthcare

Entrepreneur Mark Cuban appears before the Senate committee on modernizing health care. Read the transcript here.

Jerome Powell Speaks at NABE

U.S. Federal Reserve Chair Jerome Powell delivers the Adam Smith Award lecture in Philadelphia. Read the transcript here.

Air Traffic Controllers Union Press Conference

Air traffic controllers union hold a news briefing on the federal shutdown's impact on flights. Read the transcript here.

Fed Annouces Interest Rate Cut

Federal Reserve Chair Jerome Powell holds a press briefing after announcing a quarter-point interest rate cut. Read the transcript here.

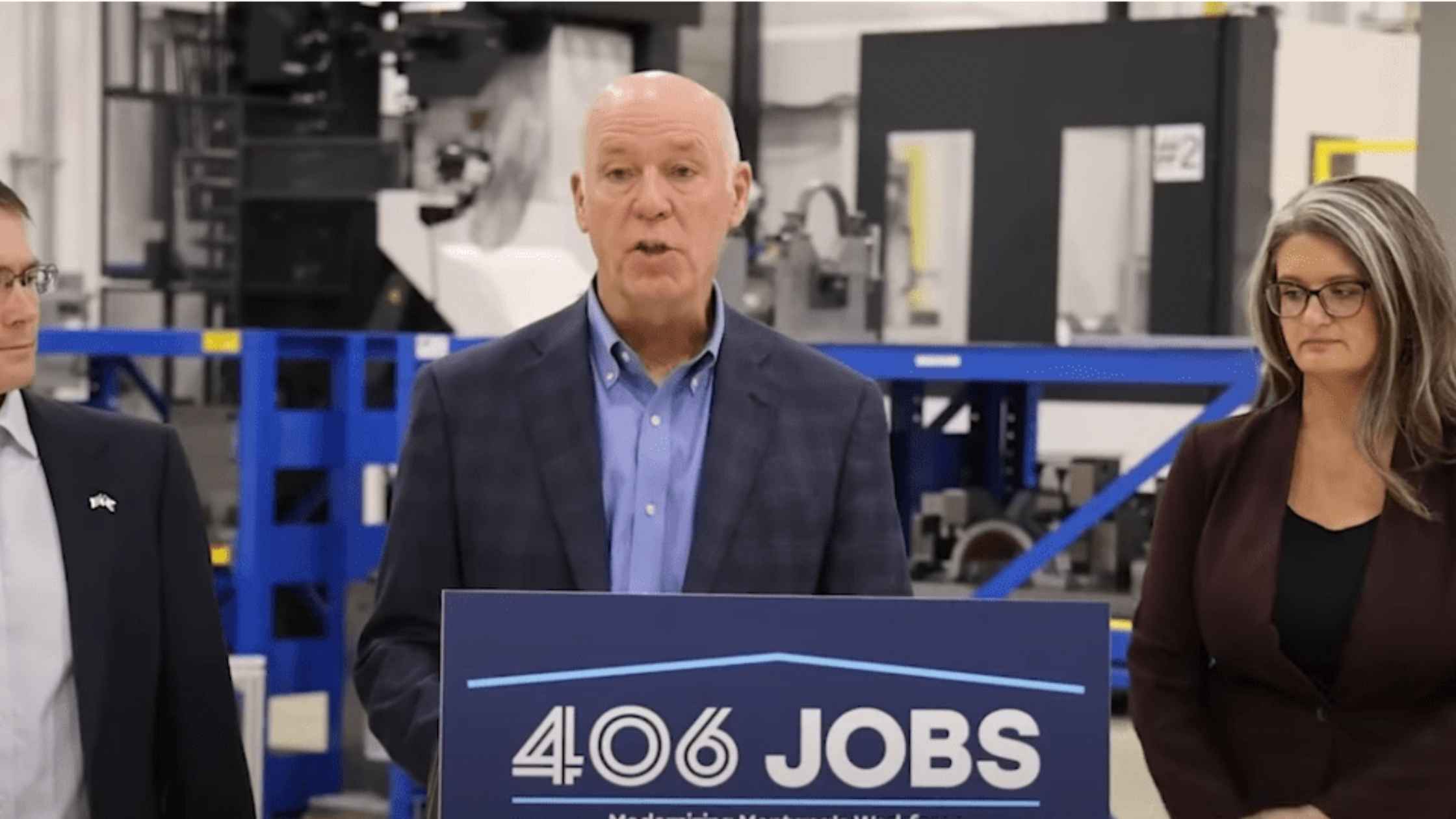

Montana Governor Expanding Workforce

Montana Governor Greg Gianforte announces a new initiative to expand Montana's workforce. Read the transcript here.

Steel Plant Press Conference

Officials hold a press briefing after an explosion left dead and injured or trapped under the rubble at a U.S. Steel plant in Pennsylvania. Read the transcript here.

Powell Press Conference on Interest Rates

Jerome Powell speaks after Fed committee decides on interest rates. Read the transcript here.

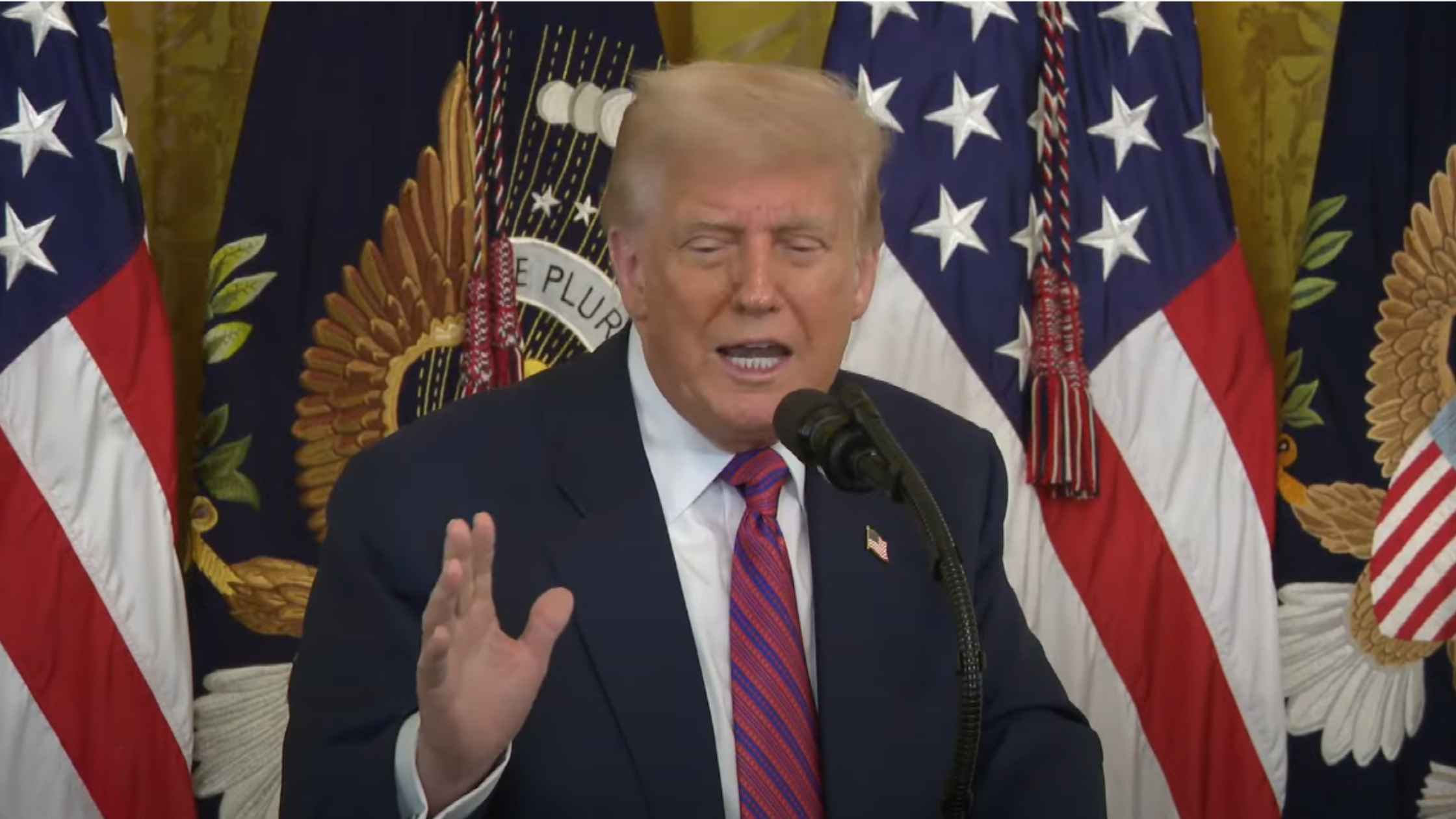

Trump Signs Crypto Bill

Donald Trump signs law creating regulations for dollar-linked 'stablecoin' cryptocurrencies. Read the transcript here.

Powell Testifies on 6/24/25

Fed Chair Jerome Powell testifies before the House committee as he warns that an interest rate cut can wait. Read the transcript here.

Apple WWDC 2025 Keynote

Apple announces all its new products and features at the WWDC 2025 keynote. Read the transcript here.

Trump Rally at U.S. Steel

Donald Trump delivers remarks at a rally to promote a deal for a Japan-based company and U.S. Steel. Read the transcript here.

NVIDIA Q1 2026 Earnings Call

$NVDA NVIDIA Q1 2026 Earnings Conference Call. Read the transcript here.

Vance Speaks at Bitcoin Event

Vice President JD Vance delivers a keynote address at the Bitcoin 2025 conference in Las Vegas, Nevada. Read the transcript here.

Trump Speaks at Saudi-US Investment Forum

Donald Trump proposes a golden age for the Middle East in a speech at the Saudi-US Investment Forum. Read the transcript here.

U.K. Trade Deal Announcement

Donald Trump and team announce a new trade deal with the U.K. Read the transcript here.

Powell Speaks on Interest Rates

Federal Reserve Chair Jerome Powell holds a news conference after an interest rate decision. Read the transcript here.

Tariff Protest Press Conference

Senate Democrats and small business owners protest tariffs. Read the transcript here.

Trump Speaks on American Investments

Donald Trump highlights investment economic accomplishments of his first 100 days in office. Read the transcript here.

Alphabet Q1 2025 Earnings Call

$GOOG Alphabet Q1 2025 earnings conference call. Read the transcript here.

Pelosi on Tariffs

Nancy Pelosi delivers remarks on the economic impact of Trump's policies. Read the transcript here.

Powell Speaks on Economy

Federal Reserve Chair Jerome Powell spoke to The Economic Club of Chicago on the state of the economy. Read the transcript here.

Subscribe to The Rev Blog

Sign up to get Rev content delivered straight to your inbox.